Housing market gets worrying update for 2026

The buyers just started disappearing.

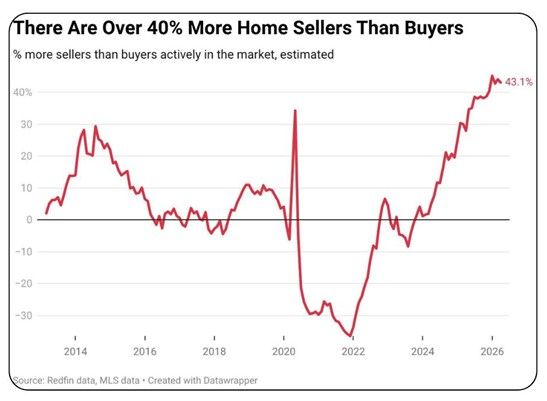

According to Redfin, sellers outnumbered buyers by 43.1% in March, up from 28.0% a year ago and just under the 45.2% record gap hit in December. That means the imbalance is still massive, even if it eased a little from the peak.

Rising mortgage rates and persistent slow sales across the U.S., even as the spring home-buying season kicks off, has pushed housing experts to lower their expectations for 2026.

National Association of Realtors (NAR) chief economist Lawrence Yun revised his 2026 forecast on Monday to project an increase in existing home sales volume of 4 percent—much lower than the 14 percent annual growth he had predicted last fall.

Redfin also says it has been a buyer’s market by their definition since May 2024.

That sounds bullish for buyers on paper.

But only for the buyers who can still afford to play.

That’s the part people miss.

This is not some glorious return to balance where average families suddenly have leverage and breathing room. It’s a market where high prices, high rates, taxes, insurance, and plain old uncertainty have thinned the crowd. The buyers who are left get more choices. Everyone else is just watching from the parking lot.

For years, demand covered up a lot.

Now the market has to function without easy money, without panic buying, and without people stretching themselves to the moon just to win a bidding war.

“Lower consumer confidence and softer job growth continue to hold back buyers,” says Lawrence Yun, NAR’s chief economist. Plus, “inventory remains a major constraint on the market. The inventory-to-sales ratio, or supply-to-demand ratio, is below historical norms.”

That changes the psychology fast.

When homes sit longer, sellers get humbled.

When buyers know they have options, urgency fades.

And when urgency fades, prices stop acting like they’re above gravity.

A lot of people still talk like it’s 2021.

The chart says otherwise.

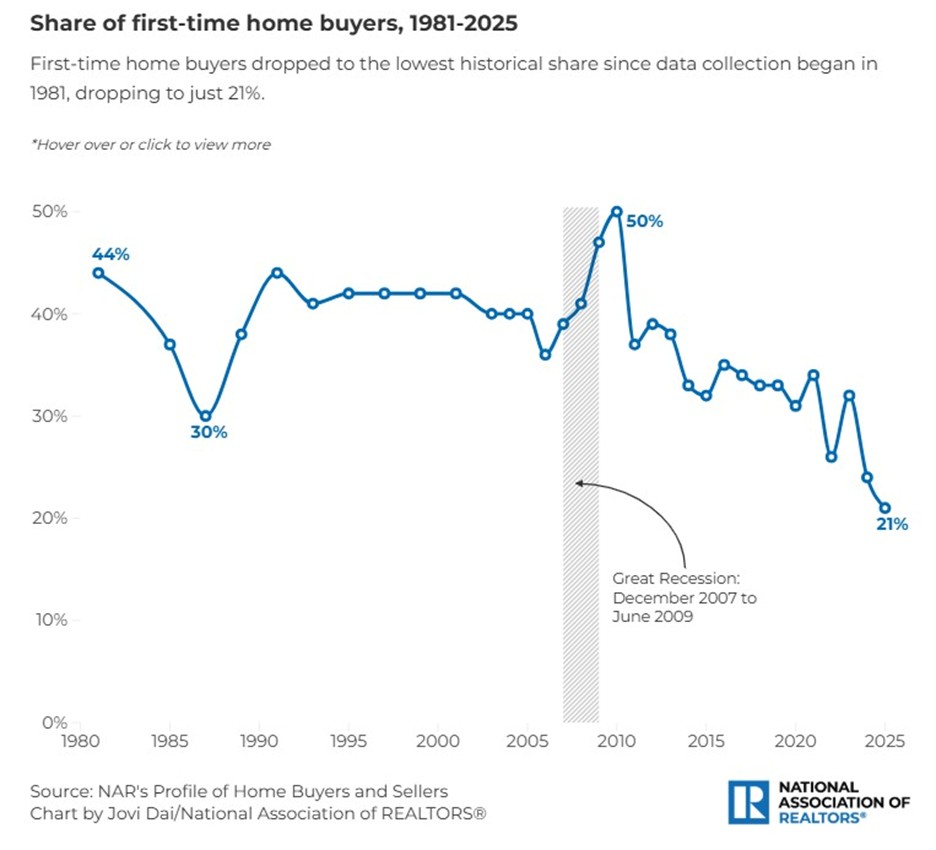

NAR has measured first-time buyers annually since 1981 and data shows them at an all-time low: 21% of primary residence buyers, vs 40% before the Great Recession. The typical first-time buyer is now 40, underscoring today’s affordability and inventory challenges.

NAR cuts sales forecast for 2026

The National Association of Realtors (NAR) has recently downgraded its sales forecast for 2026, reducing the expected increase from 14% to just 4%. This adjustment reflects a significant shift in the housing market, where mortgage rates have risen, inventory is tight, and affordability remains a challenge for buyers. The revised forecast highlights the need for a balanced market with a supply of around five to six months to facilitate buyer activity. The NAR's Chief Economist, Lawrence Yun, emphasized the importance of mortgage rates remaining lower for a prolonged period to stimulate sales activity. The market's slow start to the spring buying season and the lack of buyer activity have led to this downgrading, indicating a need for recalibration in real estate practices to align with the current market conditions.

Locally, Inventory Jumps 29% as Rising Mortgage Rates and WA State’s Tax Environment Stall Sales

- Inventory up 29%

- Brokers added 10,035 new listings just in March alone.

- Sales barely move (Up just 0.2%)

- Pending Sales (Those going under contract) decreased by 3.2%

- Prices down 1.5%

- Homes priced at $2 million or more jumped by 65% day after Millionaire Tax

A continued rise in inventory, combined with renewed pressure from rising mortgage rates, defined Washington’s housing market in March as listings climbed sharply while sales remained largely unchanged. New data also suggesting the state’s tax environment and a cooling tech sector may be pushing high-end buyers out of the market for good.

According to data released by The Northwest Multiple Listing Service (NMLS) its March 2026 Market Snapshot shows active listings surged 29.3% year over year to 15,049 homes while closed sales barely budged, rising just 0.2% from a year ago. The median sales price fell 1.5% year over year to $640,000. More homes are sitting on the market, prices are softening, and the buyers who once kept Washington’s housing engine running are increasingly hard to find.

I’ll close with this: For the last few years, housing has been stuck in a weird place.

Prices stayed high. Rates stayed high. And a lot of people kept acting like demand would just keep showing up anyway.

But the latest data says something changed.

In February, there were about 46.3% more sellers than buyers in the U.S. housing market. That was the largest seller-buyer gap in Redfin’s records going back to 2013.

That matters.

Because housing doesn’t stay expensive forever just because everyone got used to it being expensive.

At some point, reality starts asking a very simple question:

Who is actually left to buy?

Not who wants to buy.

Not who is watching Zillow every night.

Who can actually step in, afford the payment, cover the taxes, stomach the insurance, and still feel good about the deal?

That pool looks smaller than a lot of people want to admit. And when buyers keep pulling back while sellers pile up, price cuts usually stop being optional.

The market can ignore math for a while.

It usually can’t ignore it forever.

Categories

Recent Posts