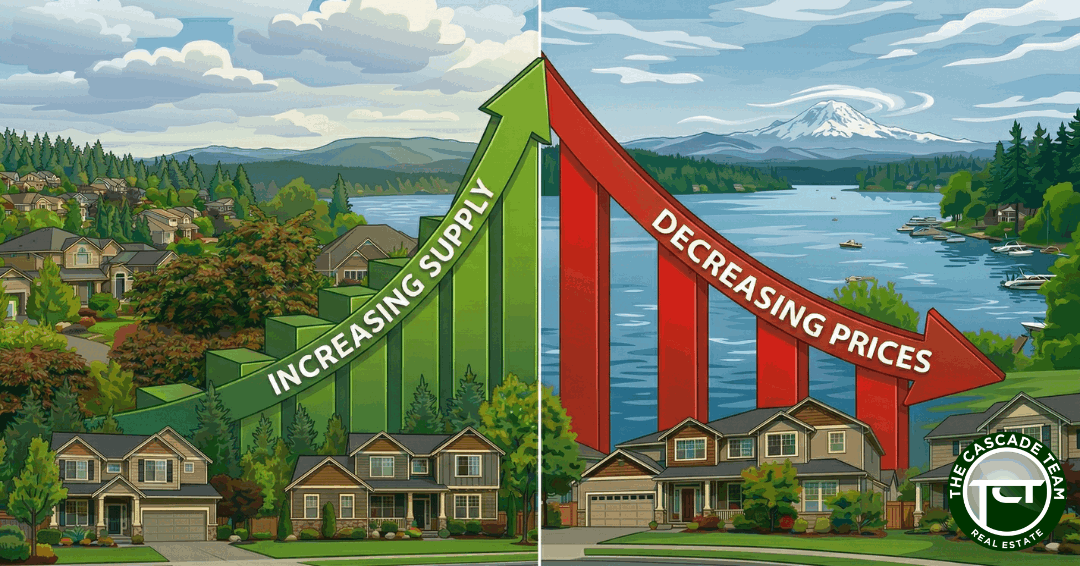

Inventory Jumps 29% as Rising Mortgage Rates and WA State’s Tax Environment Stall Sales

Inventory up 29%

Brokers added 10,035 new listings just in March alone.

Sales barely move (Up just 0.2%)

Pending Sales (Those going under contract) decreased by 3.2%

Prices down 1.5%

Homes priced at $2 million or more jumped by 65% day after Millionaire Tax

A continued rise in inventory, combined with renewed pressure from rising mortgage rates, defined Washington’s housing market in March as listings climbed sharply while sales remained largely unchanged. New data also suggesting the state’s tax environment and a cooling tech sector may be pushing high-end buyers out of the market for good.

According to data released by The Northwest Multiple Listing Service (NMLS) its March 2026 Market Snapshot shows active listings surged 29.3% year over year to 15,049 homes while closed sales barely budged, rising just 0.2% from a year ago. The median sales price fell 1.5% year over year to $640,000. More homes are sitting on the market, prices are softening, and the buyers who once kept Washington’s housing engine running are increasingly hard to find.

Active Listings

The total number of properties listed for sale increased 29.3% year over year, with 15,049 active listings on the market at the end of March 2026, compared to 11,640 at the end of March 2025. Month over month, active inventory increased by 12.8%, up from 13,341 in February 2026.

Nearly all NWMLS counties experienced year-over-year inventory growth, with 20 of 27 counties posting double-digit increases. The five counties with the largest increases were Adams (+75%), Okanogan (+58.8%), Jefferson (+53.9%), Walla Walla (+52.4%), and Snohomish (+51.8%).

The gap between supply and demand is widening rather than narrowing, and it has experts worried.

New Listings

NWMLS brokers added 10,035 new listings to the database in March 2026, a year-over-year increase of 9.5% compared to March 2025 (9,161). When compared to the previous month (February 2026), new listings increased by 35.2%, when 7,424 listings were added to the NWMLS database.

When looking at the 27 individual counties in NWMLS’s primary service area, the number of new listings increased year-over-year in 21 counties, and decreased year-over-year in 6 counties.

Mortgage rates back above 6% are crushing King County buyers

Steven Bourassa, director of the Washington Center for Real Estate Research, explained the concerns in the NWMLS report: “In a nutshell, sellers have decided that they need to get on with their lives in spite of the fact that many would be giving up low-interest-rate mortgages. However, potential purchasers cannot afford to buy.”

Mortgage rates climbed back to 6.51% by the first week of April after briefly dipping below 6% in February, driven in part by rising global uncertainty including the recent conflict with Iran, according to Bourassa. That rate spike has compounded an affordability crisis that was already severe in King County, where the median sales price reached $859,618 in March.

Pending Sales

There were 7,352 residential units & condo units under contract in March 2026, a decrease of 3.2% when compared to March 2025 (7,593). When compared to the previous month, the number of pending listings increased by nearly 25%, up from 5,886 listings under contract in February 2026.

Capital gains tax and tech sector cuts are emptying Washington of its best buyers.

Washington’s capital gains tax, passed in 2021 and upheld by the state Supreme Court, already hits high earners on investment income above $250,000. State legislators keep pushing for a broader income tax even as the Seattle-area tech sector sheds jobs and high earners look for the exit. That combination matters for housing. The buyers who could actually afford a $859,000 King County home or a $1 million San Juan County property are the same people getting squeezed by capital gains taxes, watching their stock-heavy compensation shrink, or packing up for Texas and Florida. Fewer of them are here, and the listings reflect it.

Seattle listings for $2 millions homes jump after millionaire tax

The Seattle area, being part of Washington State, has also experienced a significant increase in luxury home listings following the passage of the millionaire tax. The data from the Northwest Multiple Listing Service indicates that the number of homes priced at $2 million or more jumped by 65% the day after the tax was passed. This trend has raised concerns about a potential exodus of wealthy residents from the state. The increase in listings is not a direct result of the tax itself but rather a response to the broader market dynamics and buyer preferences.

Closed Sales

Closed sales increased by .2% year over year, with 5,417 transactions in March 2026 compared to 5,406 in March 2025. Month over month, sales increased by nearly 31%, up from 4,139 in February 2026.

Year-over-year closed sales increased in 14 of 27 counties, while 13 counties saw decreases. The total dollar value of closed sales in March 2026 was $3.8 billion for residential homes and $490.4 million for condominiums, for a combined total of $4.29 billion.

As the Iranian conflict evolves it’s adding more uncertainty to the Spring Housing Market

“We kind of had a good thing going there for about a week, and now those stars aren’t aligned. Mortgage rates are picking back up,” Windermere Principal Economist Jeff Tucker told Inman. “I’m no geopolitical expert. Iran is laying mines in the Strait of Hormuz, and this raises questions about the chances of this coming to a close anytime soon.”

“I mean, even just a couple of days ago, oil futures were very quickly improving due to news that [President] Trump had apparently signaled the conflict was done. Now, I really don’t know. We’re on this yo-yo,” he added. “But we’re early in the spring homebuying season. There’s still the chance these impacts could be limited, depending on how quickly this gets resolved.”

Even if the conflict ends tomorrow, staving off the worst-case economic and housing scenario, Tucker and other economists said elevated gas prices are likely to stick around, impacting car-dependent markets more than walkable, public transit-heavy metros.

The increase isn’t only significant at the pump but will reverberate through the cost of food and other goods. Transportation companies will need to offset the increasing cost of diesel, which has risen to an average of $5.11 per gallon. Crude oil is also key to manufacturing a never-ending list of everyday items, including something as simple as a plastic water bottle.

Oil underpins so much of economic activity and commerce. It’s the fuel that basically transports goods, both across the oceans, across roads, to the last mile, right to our homes, nowadays, especially with e-commerce. Everything we do anymore is heavily dependent on the cost of fuel. And so with the cost of fuel spiking the way it has, it’s very likely to impact, ultimately, our individual and household bills.

Beyond putting more pressure on consumers’ pockets and sentiment, First American VP and Deputy Chief Economist Odeta Kushi said rising gas costs could also impact the housing market through higher material costs for homebuilders and higher inflation. If the conflict drags on through the spring and summer, Kushi said, the Federal Reserve may feel more pressure to control “inflation dynamics.”

“Monitoring key inflation reports like the [Personal Consumption Expenditures Price Index] and the [Consumer Price Index] is important. Those two key aspects of the economy will give a better understanding of what the Federal Reserve is likely to do with monetary policy,” she said. “The Fed will need to do a balancing act to keep inflation stable, alongside maintaining full employment on the labor market side.”

The ongoing oil crisis complicates the balancing act Kushi mentioned. The Windermere economist said it’s difficult to know what the Fed will do, whether it’s holding off on planned rate cuts or actually “jacking up” interest rates. “It’s not everyone’s favorite,” he said of the option to raise rates. “But it’s the cure for a demand shock.”

Although the mere idea of the Fed raising rates is enough to fling agents and consumers out of orbit, the economists said it’s important to remember that 10-Year Treasury yields are a better predictor of what may happen with mortgage rates. And right now, despite some volatility since Feb. 28, those yields are holding relatively steady at 4.25 percent.

That’s (disappointingly) pushed mortgage rates back above 6 percent — to 6.51 percent, to be exact. But that rate is still below the 2023 peak of 7.8 percent and may be enough to keep homebuyers and home sellers who need to make a deal this spring in the market.

“I think that if we see it persist, we could start to see it impact the spring homebuying market,” Kushi said. “But right now, the 10-year Treasury isn’t moving around all that much. There’s still hope for spring. Our outlook, as we’ve been writing [reports], is more positive.”

The Market Wont Crash

At the end of the day; I don’t think that the market is going to in any way necessarily dry up, and I believe transactions will continue. I think this market could be an opportune time because when you put everything together, there have been three years of sluggish sales activity. Sellers may be more motivated than ever to make a deal. And so far, at least, the indications are that there are many more people willing to come to market with properties this season.

For sellers, prices are moving downward slightly buy not falling off a cliff as in 2008.

For buyers, there are more options and sellers are more willing to negotiate.

The coming market is going to be about finding the balance for buyers and sellers.

Categories

Recent Posts